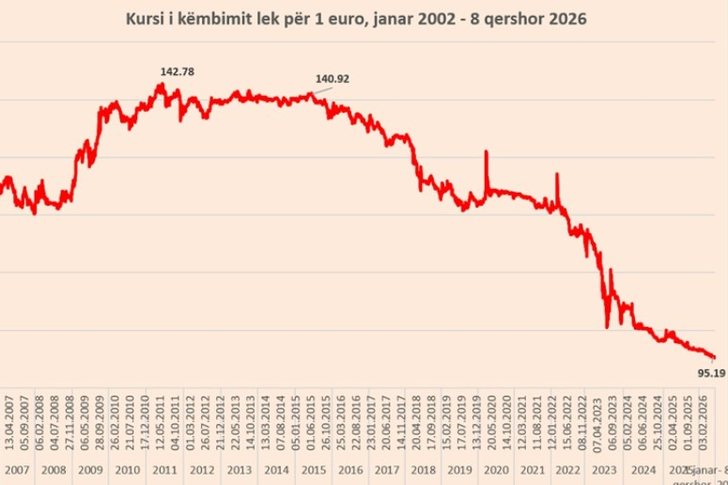

Exchange rate, June 10, 2026

This Wednesday, one US dollar is bought for 81.6 lek and s...

The non-performing loan ratio returned to decline in April. According to statistics from the Bank of Albania, the non-performing loan ratio fell to 3.75%, from 3.85% in March. This indicator continues to decline on an annual basis, compared to the level of 4.03% in April 2025.

The non-performing loan ratio is currently at its lowest level in the last 18 years.

In absolute terms, the stock of non-performing loans is estimated at approximately 36.3 billion lek. However, bad loans in value have increased by 3.4% compared to the previous year.

For the time being, the non-performing loan ratio appears to be continuing its downward trend, despite concerns related to the rapid growth of lending in recent years. The good macroeconomic performance and the continuous expansion of the loan portfolio are positively affecting the performance of the overdue loans indicator.

At the end of April, the outstanding credit to the economy reached 968.2 billion lek, an increase of 9.5 billion lek compared to March. On an annual basis, the credit portfolio to the economy is up 11% compared to a year earlier.

The measures taken last year by the Bank of Albania seem to have started to have an effect in slowing down lending for housing purchases by individuals. However, this slowdown has been offset by growth in the consumer credit segment and acceleration in the growth of the business loan portfolio.

The sector is maintaining a positive performance in terms of growth, but also financial performance and asset quality.

The crisis in the Middle East and the increase in fuel prices have put some new risks in perspective, but nevertheless the extent of the impact of this crisis seems to be more limited than could have been thought in the first period of its outbreak.

Inflation is rising and making an increase in interest rates more likely in the coming months, but Central Banks in their baseline scenarios do not foresee dramatic effects and long-term deviations from their inflation targets.

Higher interest rates would negatively affect the solvency of liabilities, but also the demand for new loans. Theoretically, this could increase the risks of an increase in problem loans, but, as long as the increase in rates is limited, this impact is not expected to be very large./Monitor

This Wednesday, one US dollar is bought for 81.6 lek and s...

The 2025 turnover reassessment for businesses in Tirana ha...

Predictions of a severe oil shortage this summer have not ...

Improving the performance of public parking lots in Vlora,...

Inflation has increased in May, rising to 3% compared to 2...

Exchange rate, June 8, 2026 This Tuesday, one US dollar is...

At the end of 2025, for all euro area members, more than 9...

Kursi i këmbimit mes euros dhe lekut e ka nisur javën në r...

The construction sector is going through a challenging per...

This Monday, one US dollar is bought for 81.8 lek and sold...

The tourist apartment market is continuing to expand at a ...

The number of properties sold by entities monitored by the...

The automotive industry in Albania is currently at a turni...

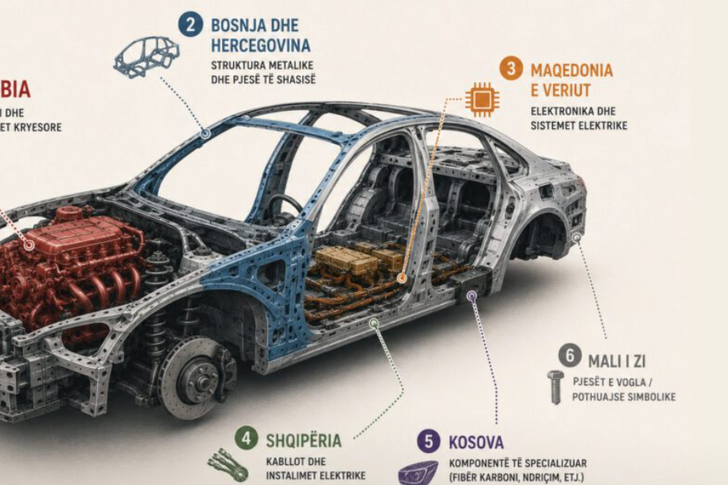

If you were to follow the industrial map of the Western Ba...

The Transparency Board, in today's meeting, decided to red...

This Saturday, one US dollar is bought for 81.4 lek and so...

Despite years of efforts at regional cooperation and free ...

Albania is the country with the highest level of severe ma...

This Friday, one US dollar is bought for 81.3 lek and sold...

The government aims to transform the country's industrial ...

Dritan Prençi is the SPAK prosecutor who is sleeping on th...

The in-depth investigations that SPAK conducted into Ajola...

SPAK's standards, the way it investigates, how it secures ...

Irfan Hysenbelliu claims to be a big businessman, an hones...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

A road accident was recorded a few minutes ago on the Pogr...

The State Police has published new footage from the operat...

A TNT explosion has occurred in the village of Balldren i ...

Gunfire broke out this morning in Lezha. According to repo...

Albania is facing a deep demographic crisis where official...

This Wednesday, our country will be affected by relatively...

The UN's World Meteorological Organization now warns that ...

Intense rainfall has caused numerous problems in the Radom...

Billionaire Bill Gates will appear today before a US Congr...

Pope Leo XIV visited one of Spain's largest prisons on Wed...

US President Donald Trump said Iran's military has been "t...

The Greek government is proposing the new European framewo...

Korça has transformed this weekend into the capital of cel...

Korça is ready to open the summer season with one of the c...

Two years after his passing, the renowned Korçë poet Skënd...

The Ethnographic Museum of Berat has opened its doors to v...

The non-performing loan ratio returned to decline in April...

This Wednesday, one US dollar is bought for 81.6 lek and s...

The 2025 turnover reassessment for businesses in Tirana ha...

Predictions of a severe oil shortage this summer have not ...